The Race Window

Iran cannot outlast the clock. The question is whether a recession breaks the US first.

The headlines this week have been a masterclass in whiplash. Friday morning, Iran’s Foreign Minister Abbas Araghchi posted on X that the Strait of Hormuz is “completely open” for all commercial vessels. Minutes later — and I mean minutes — Trump responded on Truth Social with two posts in sequence. The first thanked Tehran. The second clarified that the US naval blockade “WILL REMAIN IN FULL FORCE AND EFFECT AS IT PERTAINS TO IRAN, ONLY, UNTIL SUCH TIME AS OUR TRANSACTION WITH IRAN IS 100% COMPLETE.” Later reports of IRGC denying this opening so long as naval blockade exists. This morning the IRGC seemingly targeted a cruise ship.

Bloomberg called it a breakthrough. NBC called it a ceasefire test. Al Jazeera called it contradictory. The S&P printed an all-time high. Brent dropped 9%. WTI dropped 11%. VLCCs queued up at the strait entrance, hesitated, and most turned around.

The market wanted to price peace. The market got something else.

Here is the reality sitting underneath the announcements: a handful of cargo ships and one bitumen tanker exited the Persian Gulf on the day Iran declared the strait open. Zero oil tankers. The announcement didn’t move ships. The announcement moved a short position that somebody placed on Brent futures twenty minutes before Araghchi’s post — 7,990 lots, roughly $760 million notional — which the CFTC is now investigating as the third suspiciously timed macro trade ahead of a Middle East policy announcement in recent weeks.

The strait is open on paper. The strait is closed on the water. And somewhere between those two facts, the economic strangulation phase of this war has already begun.

The phase change nobody is pricing

Operation Epic Fury opened on February 28 with surprise airstrikes. It progressed through a fourteen-day bombing campaign, a two-week ceasefire that Iran violated by charging tolls on Hormuz transits, a second round of failed Islamabad talks, and a full US naval blockade of Iranian ports beginning April 13. What happened this Friday is the third phase: a choreographed opening that restores commercial shipping to non-Iranian Gulf states while leaving Iranian exports completely shut off.

This is the architecture Washington is trying to build. An “open” Strait of Hormuz where enforcement is easier, Iran’s export capacity is permanently damaged, the shadow fleet is observable, and the global energy system tilts toward American barrels and American LNG. Nothing about this is accidental. It is the one outcome the US can live with in this war, and they are pushing toward it until they either get it — or a recession stops them first.

The question that matters now is not whether the strait reopens. The question is who can withstand economic damage longer. And when you run the numbers, it is not close.

Iran’s revenue is collapsing from a position that was already compromised

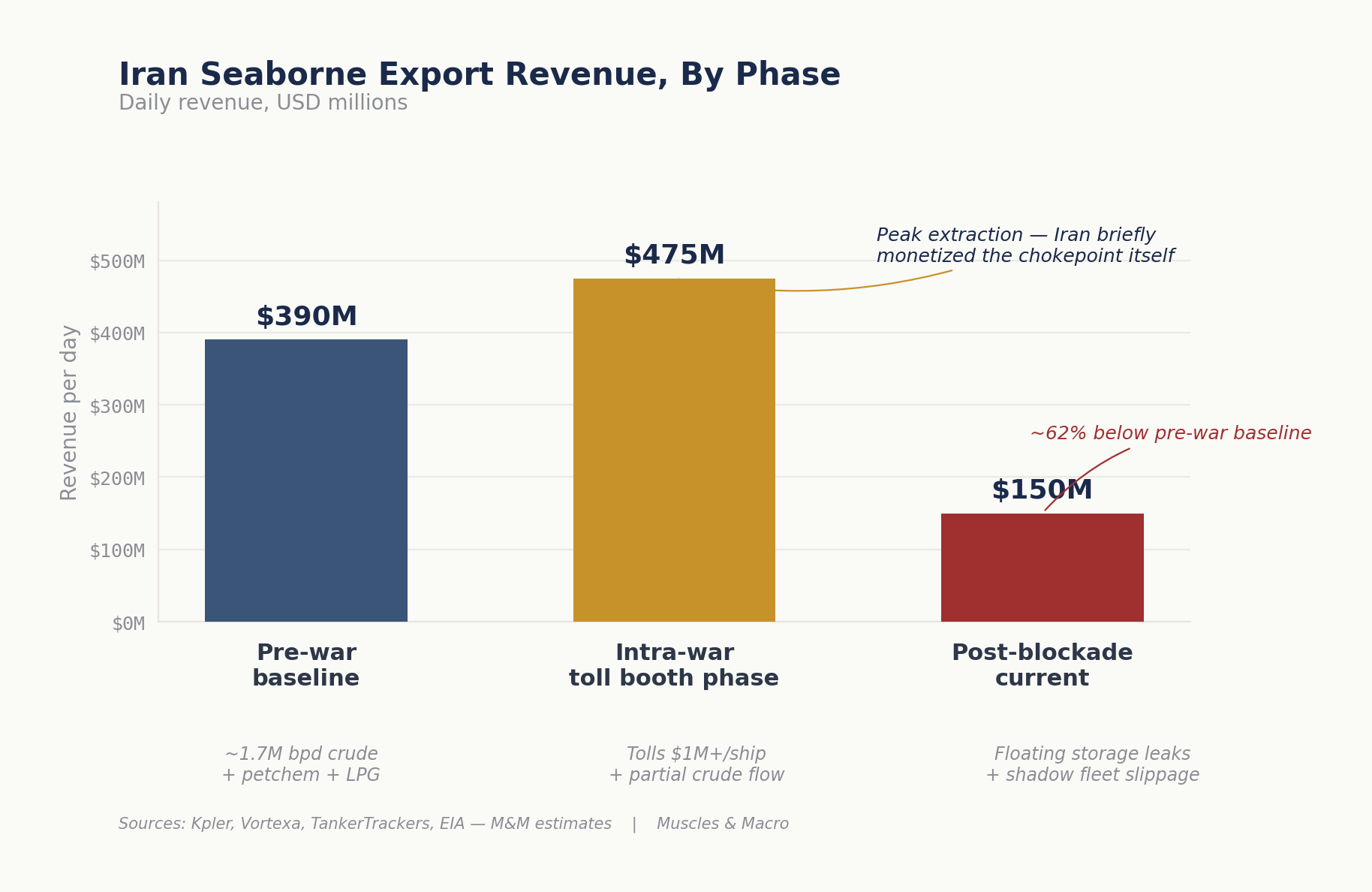

Before the war, Iran was shipping roughly 1.5 to 2 million barrels per day of crude oil, plus petrochemicals, condensates, and LPG products, for total seaborne export revenue in the range of $350 to $430 million per day at prevailing prices. Call it $390 million a day as a reasonable midpoint. That is the baseline.

When the war started and Iran effectively closed the strait, something unexpected happened. During the two-week ceasefire in early April, Iran began controlling traffic through the chokepoint and charging tolls of over $1 million per ship. Combined with partial crude flow to Chinese buyers willing to accept the risk premium, Iran briefly pulled in more revenue during the toll booth phase than during peacetime. This is the part of the war analysts have struggled to reconcile with the “Iran is losing” narrative. For a few weeks in early April, Iran was winning the cash flow fight by turning sovereignty over Hormuz into a billable service.

Then the Islamabad talks failed. Then the US Navy blockade took effect. Then Iran’s revenue fell off a cliff.

Current blockade-phase revenue is running somewhere between $100 and $250 million per day — a blend of floating storage drawdowns, a handful of shadow cargoes slipping past enforcement from Kharg and Bandar Abbas, and some continued product trade through non-oil channels. Call it $150 million a day. That is 62% below the pre-war baseline and 68% below the toll booth peak. At the monthly level, Iran has gone from $11.7 billion to $4.5 billion in seaborne export revenue. The gap is $7 billion per month in lost dollar inflows against a domestic economy that the IMF projects will contract 6% this year.

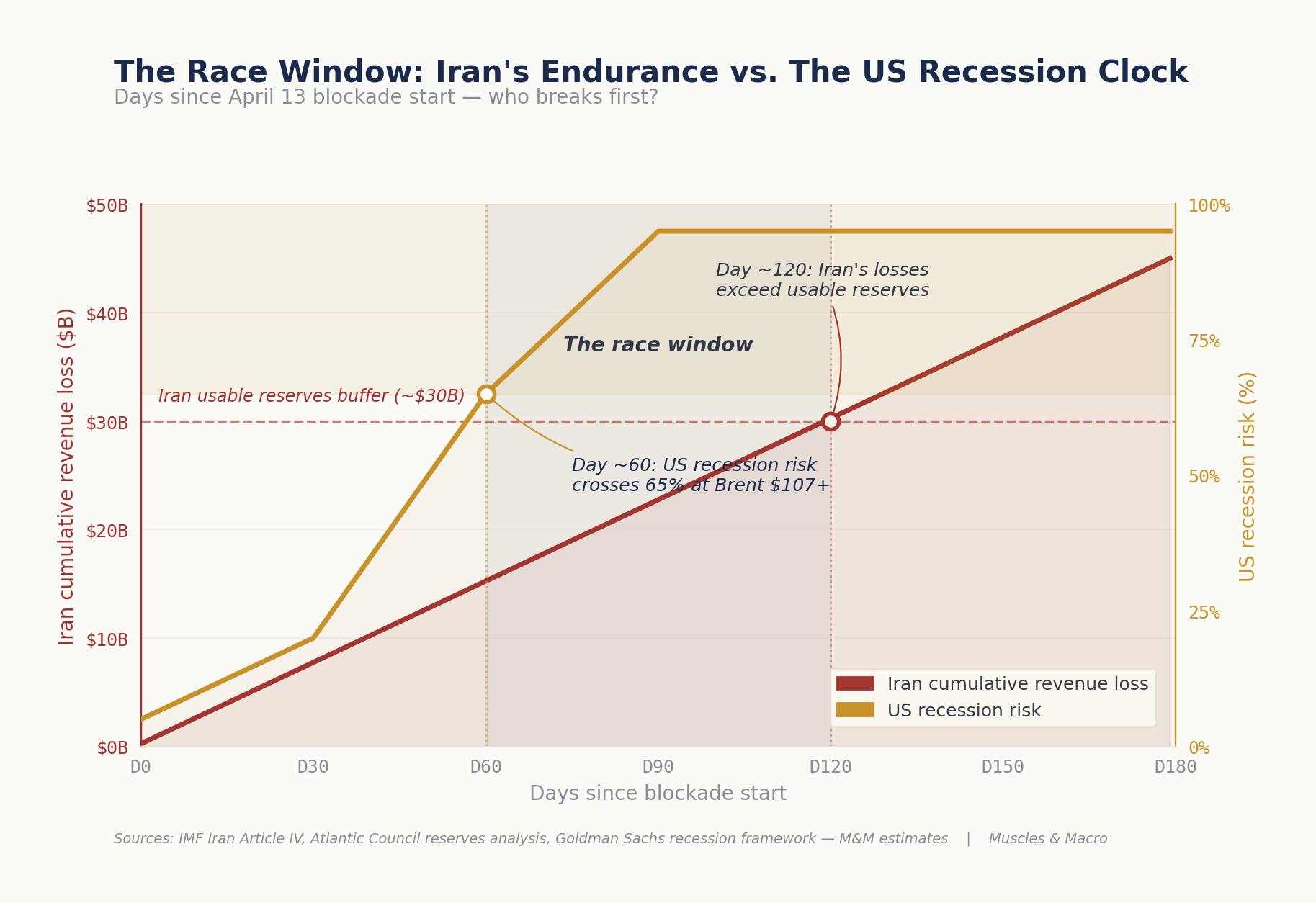

This matters because revenue is not the same as reserves. Iran’s headline foreign reserves figure sits somewhere between $80 billion and $110 billion depending on whose accounting you trust, but the usable portion — currency Iran can actually access and deploy to stabilize domestic prices, pay import bills, and defend the rial — is much smaller. Sanctions and foreign asset freezes have restricted most of the notional reserves. Atlantic Council analysis and IMF Article IV reviews put actual usable reserves at around $30 billion, with the rest held in jurisdictions that require political permission Iran does not have.

At a loss rate of $250 million per day, that $30 billion buffer runs out in roughly 120 days. If the loss rate compresses toward $150 million a day as enforcement leakage continues, the buffer stretches to 200 days. Neither number is long.

The US is making money because the war made the math asymmetric

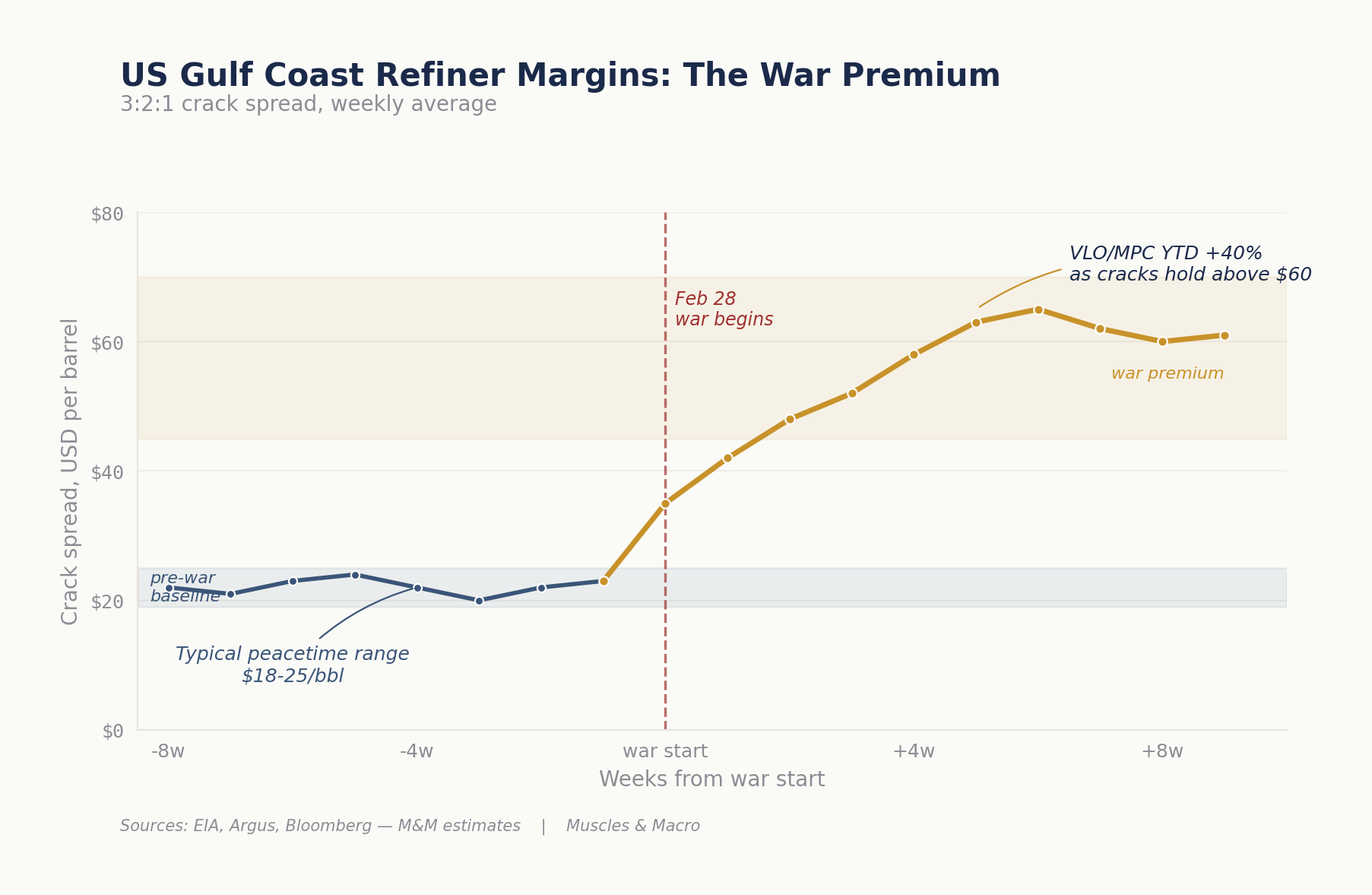

Meanwhile the US energy complex is running in the opposite direction. American oil does not cross Hormuz. When fear spikes in the Middle East, more buyers quietly reroute demand into the US system — Permian crude, Bakken crude, Canadian heavy coming down through Enbridge and Keystone, Mexican Maya shipped up from Campeche. US Gulf Coast refiners source that cheaper feedstock domestically and regionally, then sell diesel, jet fuel, and gasoline back to Europe and Asia at war-level crack spreads.

The spread is the entire game. Before the war, the US Gulf Coast 3:2:1 crack spread ran in a typical peacetime range of $18 to $25 per barrel. That is the normal margin between what a refiner pays for a barrel of crude and what it receives for the refined products that come out the other side. It is the single most important number in understanding why a Middle East war turns out to be a transfer mechanism rather than a cost.

Within a week of Epic Fury beginning, the spread jumped to $35. Within a month it crossed $50. By early April, with Hormuz uncertainty fully priced and European product inventories drawing hard, the spread printed above $65. It has held in that war premium zone ever since. VLO and MPC — the two purest plays on Gulf Coast refining capacity — are up more than 40% year-to-date. CVX and XOM are up on the supply side of the same trade. This is not speculation. This is a structural margin expansion driven by a supply chain that terminates in places Iranian missiles cannot reach.

The LNG side of the business is running the same playbook. With Qatar’s North Dome offline or politically risky, with Ras Laffan facing a three-to-five year recovery timeline, US LNG exporters are running flat out — Sabine Pass, Corpus Christi, Freeport, Cameron, Calcasieu Pass, Plaquemines, Cove Point. Export capacity sits above 14 billion cubic feet per day and every cargo is spoken for. European utilities that spent three years trying to diversify away from Russian pipeline gas are now structurally dependent on American molecules priced at oil-linked spot levels. Long-term contracts that would have been politically impossible in peacetime are being signed quietly right now.

Every extra day of Hormuz risk compounds this. Iran gets poorer. The US energy complex gets richer. The trade is not subtle — it is visible in the equity prices, the freight rates, the LNG term contract flow, and the widening product spreads.

But there is a catch. The math only works while the US consumer can absorb the gasoline price that comes with Brent in the $100s.

The recession clock is the only constraint that matters

At Brent above $107 per barrel sustained, US retail gasoline prices cross the threshold where consumer discretionary spending starts to compress in a self-reinforcing way. Historical consumption data, credit card transaction panels, and CPI passthrough studies all converge on the same figure: somewhere between two and three months of sustained Brent pricing above that band, the damage to consumption outgrows the energy sector’s boost to GDP. The refiners are still making money. The producers are still making money. But the broader economy is already sliding.

This is where the imperial calculus of Epic Fury meets its one hard limit. Washington can tolerate Iran’s collapse. Washington cannot tolerate its own recession. And the two timelines do not match up the way the White House needs them to.

The math is straightforward. Using Goldman Sachs’ framework for oil-price-driven recession probability, the US recession risk at current Brent levels crosses the 65% threshold around day 60 of sustained pressure and approaches certainty by day 90. The Iranian reserves buffer breaks around day 120. The gap between those two points — roughly day 60 to day 120 — is the race window. That is the period during which the US is absorbing real domestic economic damage while Iran has not yet been forced to the negotiating table.

Every day inside that window costs the administration political capital it cannot replace. The CPI print from June and July will arrive before the midterm cycle starts in earnest. The Fed’s September meeting will land in the middle of the gasoline-pain window. The Treasury’s October refunding announcement will land while consumer confidence is cratering. None of these are theoretical. They are known events on known dates, and they all sit inside the race window.

The one outcome Washington cannot afford is a scenario where Iran outlasts the clock. If the blockade enters month four with Iranian exports still leaking at $150 million a day, the White House faces a choice between a deal that formally preserves Iran’s export capacity and a recession that arrives six weeks before midterms. That is why the Araghchi opening announcement this Friday happened on the same day Trump said a deal is “very close.” The pressure is not about Iran’s reserves. The pressure is about the US political calendar.

The one leak in the thesis

The framework I have laid out here is directionally correct but it has one important caveat that honest analysis requires naming. The liquidity warfare pillar of this campaign is not working the way it was designed to work. Russia is currently earning around $600 million per day from crude exports because the Urals discount has collapsed, Bessent issued a 30-day sanctions waiver that is about to be renewed, and Chinese buyers are paying premium prices for Russian barrels that cannot move anywhere else.

This is the one part of the war where the script has flipped. The US is extracting revenue from Iran while simultaneously enriching Russia. The longer the race window stays open, the more Moscow banks. From a strategic optics perspective, this complicates the moral framing of the campaign. From a thesis perspective, it means the financial warfare tools the US assumed would work against the full Iran-Russia-China axis are leaking in the direction that matters most for Ukraine. China’s deepening ties with Iran and Russia through CIPS settlement, ruble-yuan energy trade, and shadow fleet registries suggests the parallel system is maturing faster than the enforcement stack is tightening.

None of this changes the core asymmetry between the US and Iran. Iran cannot outlast the clock on its own balance sheet. But the broader claim — that this war strengthens US hegemony on every axis — needs the Russia qualifier attached, honestly, for the analysis to hold together.

The endgame on paper

The closer matters. Washington is not trying to return Hormuz to the status it had on February 27. They are trying to architect a new equilibrium where the strait is open, but the terms of access are permanently different. In the version Washington wants, sanctions become easier to enforce because physical shipping is now tracked through a tighter compliance stack. Iran’s export capacity is permanently dented. The shadow fleet is smaller, more expensive to operate, and continuously targeted. The global energy plumbing tilts incrementally toward American oil and American LNG. The franchise states that compose the intermediary layer — India, UAE, Turkey, Brazil — are bound tighter to US market access because the enforcement infrastructure is tighter and their own hedging space is narrower.

That outcome is achievable if the race window closes in Washington’s favor. If Iran runs out of reserves before the US consumer runs out of patience, the deal gets signed on US terms and the endgame locks in. If the US consumer runs out first, the deal gets signed on terms that formally preserve Iranian capacity, the enforcement architecture weakens, and the strategic gains from the war erode even as the financial gains for refiners and LNG exporters persist.

The honest answer to “how does this end” is that nobody knows yet. The framework is clear. The balance sheet math is clear. The political constraint is clear. What is not clear is which side hits its breaking point first, and the clock on both sides is counting down in real time.

The signal I am watching is not the announcements. The signal is ship traffic in the strait. When VLCCs start flowing in normal volumes — not a handful per day but the pre-war baseline of thirty-plus — then a deal exists. Until then, the strait is open in press releases only, and the economic strangulation continues. Every day that continues, the asymmetry compounds in one direction while the recession clock compounds in the other.

The race window is where the war actually gets decided. Everything else is noise.

Muscles & Macro analyzes geopolitical, macro, and energy developments through a structural framework. Nothing in this article constitutes investment advice. All content is for educational and entertainment purposes. The author may hold positions in securities discussed as part of personal analytical research.