The Third Layer: AI's Useless Without a Body, and the Body Is Chinese

A framework update on the AI race the consensus is missing

The piece nobody talks about

The AI race gets covered as a contest over two layers. Chips on one side. Energy on the other. The US owns the chips. China owns most of the energy. Everyone watches that scoreboard.

There is a third layer. Almost nobody watches it. China owns it.

Without robots actually performing physical tasks, the ultimate result of AI never lands. The frontier models are remarkable. The compute infrastructure is the largest capital build in industrial history…and the chip wars are absolutely real. None of it produces a single physical good without something to do the work.

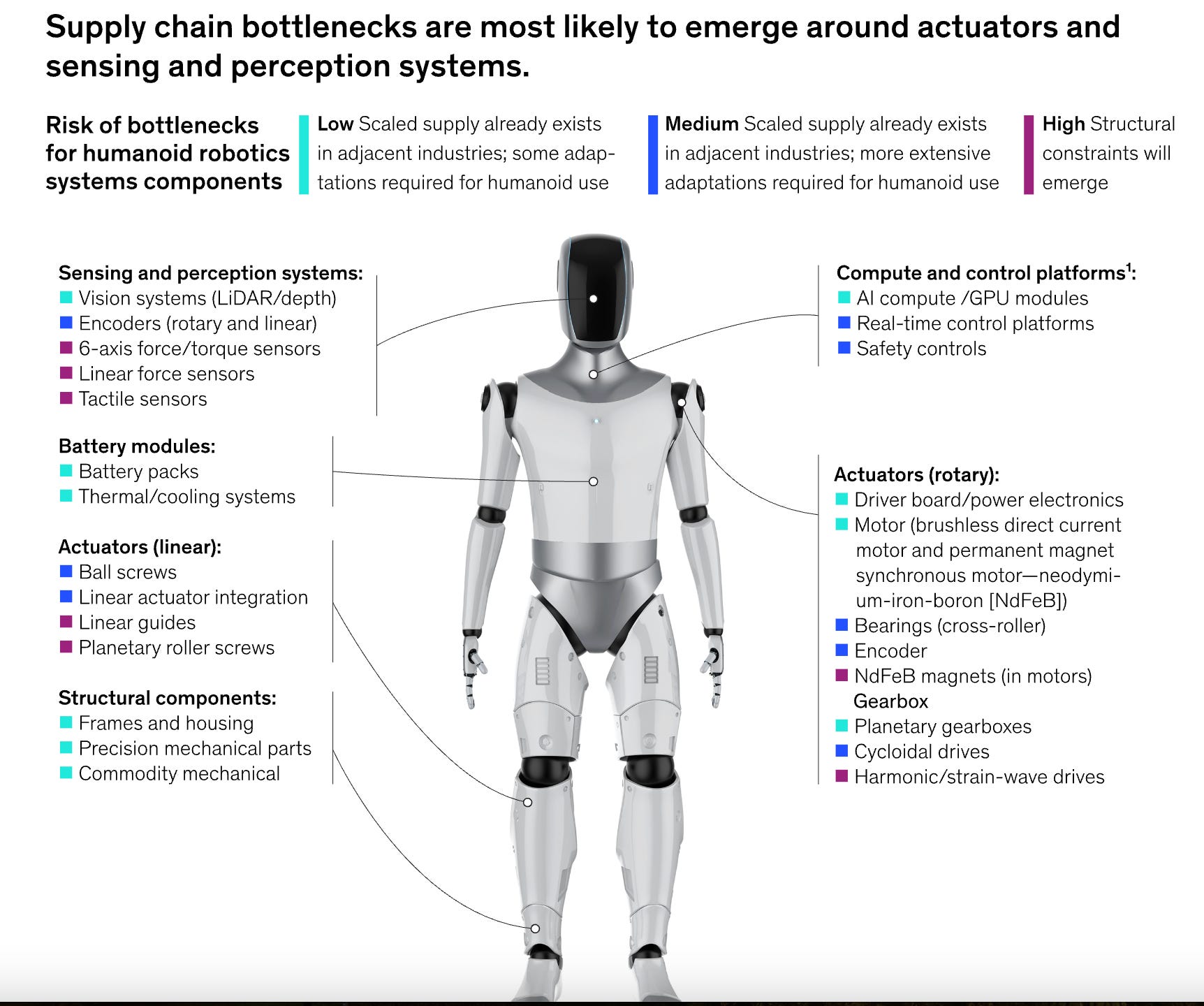

That something is humanoid robots, factory automation, autonomous logistics. The bridge between intelligence and economic value. The thing that turns model output into GDP. The supply chain that makes any of that work is 90% Chinese.

This is the third clock in the framework. The chip clock and the power clock have been the architecture for two years. The deployment clock joins them now.

Source: McKinsey & Company, "Turning humanoid supply chain constraints into billion-dollar wins," McKinsey Industrials Insights.

What the framework already says

The Muscles & Macro thesis has been a two-clock model. The chip clock measures how fast China closes the silicon gap — Huawei Ascend, SMIC 7nm, CXMT HBM, DeepSeek-class model diffusion. The power clock measures how fast the US closes the energy gap — gas peakers, SMRs, transformer supply, grid expansion. Both clocks run toward the Goldilocks Window of 2027 to 2030 when Taiwan’s silicon shield is at maximum vulnerability.

The framework has been clear on something else. China is the prior comprehensive deployer of Pillar 1, 1 of 4 pillars my Youtube Tentpole video will cover— supply chain control at continental scale. Efforts within this Pillar include The Belt and Road infrastructure, the Africa critical minerals architecture, the Latin America lithium positioning. American Imperialism 2.0, a thesis im always mentioning, is catch-up against a position China already holds. Think Greenland rare earths, Venezuela crude flow redirection, Cuba secondary sanctions, these are partial recoveries of leverage that was structurally Chinese for the prior decade.

What the framework had not fully absorbed until this update: the same prior-deployer dynamic operates inside the AI race itself. The third layer — embodiment — was built out at Chinese scale while the US was building Silicon Valley.

Source: McKinsey & Company, "Turning humanoid supply chain constraints into billion-dollar wins," McKinsey Industrials Insights. McKinsey Battery Insights; McKinsey Center for Future Mobility; McKinsey Global Energy Insights.

The structural finding

The US owns the silicon stack. Advanced chips at TSMC and Intel 18A. EUV lithography from ASML. High-bandwidth memory from SK Hynix, Samsung, Micron. These are the inputs to AI compute.

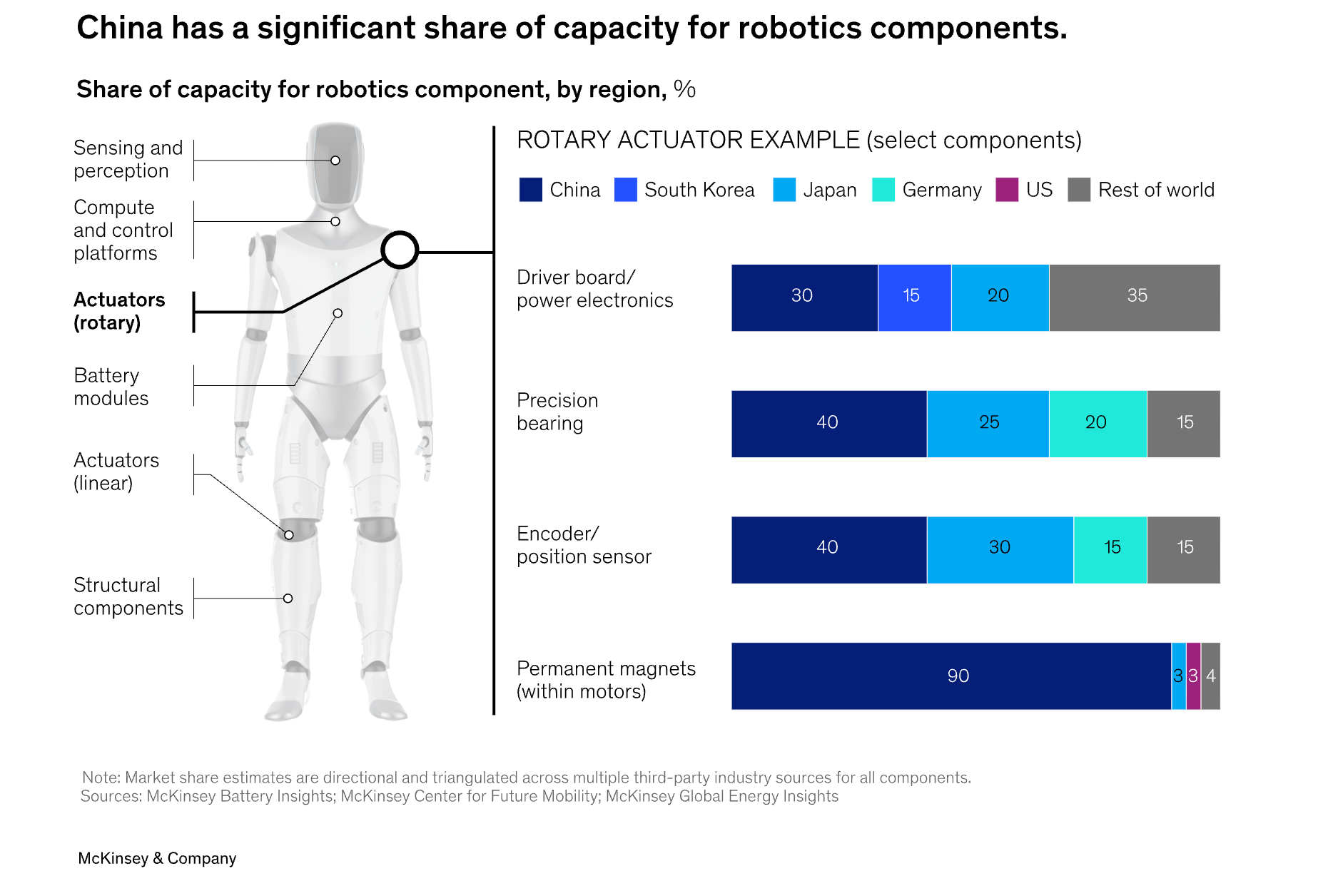

China owns the embodiment stack. Rare earth magnets. Servo actuators. Harmonic and cycloidal reducers. Force-torque sensors. Precision gearing. Battery integration. Frame machining. These are the inputs to AI deployment.

Both stacks are physical chokepoints. Both have tacit-knowledge moats with decade-plus replacement timelines. Both gate something essential. The audience that knows the chip race has not yet absorbed that the embodiment race has the same structural shape with the country labels reversed.

The Silicon Wall has a mirror. The mirror is Chinese.

How dominant is dominant

The numbers tell the story.

Rare earth processing is approximately 90% Chinese. That number has been repeated for years and remains accurate. McKinsey’s 2024 critical minerals analysis puts Chinese refining share at 90% for heavy rare earths specifically — the dysprosium, terbium, samarium, gadolinium category that makes a humanoid actuator’s magnets withstand operating temperatures.

NdFeB sintered magnet manufacturing is approximately 91-94% Chinese per Adamas Intelligence. The technology was developed in the US and Japan in the 1980s. Production migrated to China through the 1990s and 2000s as Western firms exited on environmental compliance costs and Chinese state-supported capacity. The exit was complete enough that the US has had near-zero domestic NdFeB production capacity until MP Materials’ Independence facility came online at industrial scale in Q1 2026.

Each humanoid robot needs approximately one kilogram of NdFeB magnets per Adamas Intelligence supply chain analysis. At 13,000 humanoids shipped globally in 2025 and Morgan Stanley’s projected 28,000 in 2026 China alone, that’s 13,000 kg in 2025 scaling toward 50,000+ kg in 2026 just for humanoids — on top of the 200,000+ MT/year that already goes to EV motors, wind turbines, consumer electronics, and industrial automation.

Actuators are more nuanced but the picture is the same. The Yangtze Delta has emerged as the integrated cluster — within a 200km radius of Shanghai, every component a humanoid needs can be sourced. Suzhou for harmonic reducers (Green Harmonic on the STAR Market, Shuanghuan Transmission, Leaderdrive). Ningbo for magnets and Tuopu/Sanhua actuators. Hangzhou for Unitree’s in-house servo motors. Shanghai for AgiBot integration and force sensors. Jiangsu province for precision machining of frames and chassis. Battery pack assembly across the region.

The closest American or European equivalent does not exist. Japan has the premium tier — Harmonic Drive Systems, Nabtesco, Nidec — but Japan does not have continental-scale integration. Germany and Switzerland have Maxon and Faulhaber motors, but at lab-scale quantities. Korea has Hyundai’s Boston Dynamics integration but a thin domestic supply chain beneath it.

The Yangtze Delta is to embodiment what Taiwan is to chips. Same form of geographic concentration. Same depth of tacit knowledge. Same decade-plus replication timeline. The US has nothing equivalent. Not in 2026, not in 2027, not before MP Materials’ 10X facility commissions in 2028.

The cost gap

The clearest way to see the dependency is the cost stack on the most-discussed Western humanoid program.

Tesla’s stated target for Optimus is twenty thousand dollars per unit at scale. The current bill of materials with Chinese components, per AUTNMY’s OMEGA model and corroborated by McKinsey, is forty-six thousand dollars. Without those components — if all sourcing moved to non-Chinese suppliers using existing Western and Japanese capacity — the BOM rises to one hundred and thirty-three thousand dollars per unit.

A roughly three-times cost penalty on the flagship Western humanoid program. The penalty is steepest for Tesla because Tesla has leaned hardest on Chinese suppliers — Sanhua for actuators ($685M order placed October 2025), Tuopu for precision components, multiple smaller Chinese vendors for magnets and bearings.

Figure, Apptronik, 1X, Agility, Boston Dynamics — these programs have less direct Chinese supplier exposure on actuators (they tend to use Japanese harmonic drives and Swiss or German servo motors). But the magnet dependency is universal. There is no commercially-viable non-Chinese NdFeB supply chain at humanoid scale in 2026.

If the licenses stop, the cost penalty propagates through every Western humanoid program.

What changed in 2025-2026

The licenses have not stopped. They are, however, now sitting on the table.

China’s MOFCOM Announcement 18 in April 2025 placed seven medium and heavy rare earth elements under export license. Licenses are required for any export, including humanoid-relevant samarium, gadolinium, and lutetium. License review takes 45 to 60 days minimum. Musk noted on Tesla’s Q1 2026 earnings call that licenses for US destinations now take “at least six months” in practice.

In October 2025, MOFCOM Announcements 61 and 62 extended that license requirement to anyone re-exporting Chinese rare earth content anywhere in the world. This is the first significant Chinese extraterritorial export control — the structural mirror of US chip export controls against China since 2022. The October extension was suspended in November 2025 as part of the Trump-Xi truce. The suspension expires November 10, 2026.

The April 2025 controls remain fully in force. The October 2025 extension is paused but loaded. Both sides — US chip controls and Chinese rare earth controls — are now in a negotiated pause that could collapse on either side.

The doctrinal point matters more than the headline. Whether or not the extension reactivates in November 2026, the structural fact is established: the denial mechanism runs both ways. The US chip control playbook has been mirrored by China at the rare earth and embodiment layer. The Imperialism 2.0 doctrine’s Pillar 3 — Precision Denial — is bidirectional. China holds the symmetric weapon to what the US has been using against Chinese chip access since 2022.

This is the framework update. The thesis previously treated Pillar 3 as a US-controlled instrument deployed against China and intermediaries. The 2025-2026 receipts confirm China has built and tested the equivalent instrument. The mirror is operational.

The scale gap

Cost penalty is theoretical. Shipped units are not.

AgiBot shipped its ten-thousandth humanoid robot in March 2026. That’s cumulative — they went from 5,000 to 10,000 units in three months. AgiBot is now the global market leader in humanoid robot shipments, holding approximately 39% of 2025 global market share per Omdia data published in January 2026.

Unitree shipped 4,200 humanoid robots in 2025 per Omdia (Unitree’s own disclosure puts the number at 5,500+, with the discrepancy being a delivered-vs-shipped accounting question). Unitree is targeting 10,000 to 20,000 units in 2026 and filed for a $608 million IPO on the STAR Market in early 2026.

UBTECH shipped approximately 1,000 units in 2025. Combined with AgiBot and Unitree, Chinese humanoid OEMs accounted for approximately 80% of global humanoid robot shipments in 2025 — roughly 10,300 of 13,000 global units.

Tesla, Figure, Agility, and other Western programs shipped approximately 150 to 500 units each in 2025. Tesla has not started mass production of Optimus as of May 2026 — the Q1 2026 earnings call confirmed production starts late July or August 2026 after the Model S and X production lines are decommissioned in early May to free up Fremont capacity. Figure shipped 240 units in April 2026 alone, doubling monthly. AgiBot is meanwhile shipping at scale, and shipped more units in Q1 2026 alone than every Western humanoid program combined.

The volume gap is widening. China is not threatening to win the embodiment race. China is several years into already winning it. The framework receipt the consensus has not absorbed.

The chip-vs-embodiment asymmetry

The two stacks are not symmetrical in everything. They are asymmetrical in two ways that matter for the framework.

First, in resolution speed. The US can rebuild non-Chinese rare earth processing faster than China can rebuild non-Taiwan advanced logic fabrication. MP Materials’ 10X facility is on a 2028 timeline. ASML EUV equivalency in China is on a 2030-plus timeline. Energy Fuels heavy rare earth commercial production is targeting Q4 2026. SMIC’s most advanced node is still 5-7nm-equivalent versus TSMC’s 2nm. The chokepoints have different replacement durations and the US side may have the shorter one.

Second, in deployment dependency. The chip race is gated on the cutting edge — frontier models need leading-edge silicon. The embodiment race is gated on commodity scale — humanoids and industrial automation can use 90nm chips and don’t need the bleeding edge. The chip stack is a vertical hierarchy with a few suppliers at the top. The embodiment stack is a horizontal cluster with thousands of integrated firms. Different structural shape, different resolution path.

These asymmetries matter because they change the conclusion. The framework finding is not “China wins the AI race because it owns embodiment.” The framework finding is “the AI race has two physical chokepoints, the US owns one and China owns the other, and the relative resolution speed of each chokepoint determines the outcome by 2030.”

The Goldilocks Window the framework has been pointing at for chips and energy now extends to embodiment. Three clocks instead of two. The race is more bifurcated than the consensus assumes.

Connection to the broader Imperialism 2.0 thesis

For readers following the broader M&M framework, the embodiment finding extends Imperialism 2.0 in two specific ways.

The Allied Incidence Problem deepens. Japanese, Korean, and European humanoid programs depend on Chinese magnet supply just as much as American programs do. There is no Western humanoid stack that can be cleanly separated from the Chinese embodiment chokepoint. The same way Iran sanctions imposed maximum allied pain in Japan and South Korea via Hormuz dependency, embodiment sanctions or export controls would impose pain on every Western humanoid program simultaneously. The allied vulnerability is structural.

The tier framework extends. The framework has categorized targets as satellites, intermediaries, active counter-positioners, and peer competitors. The embodiment finding suggests China occupies the Active Counter-Positioner role at the deployment layer specifically — not just buffering against US Pillar 3 with stockpiles (the Iran-era pattern) but building symmetric structural alternatives that operate against the US. The October 2025 MOFCOM extraterritorial extension is the receipts. China is no longer just absorbing American chip controls. It has built and tested the mirror.

Names exposed to this framework

Below is a layer-mapped list of names with exposure to the structural thesis. This is framework analysis, not portfolio recommendation. Every name is included on the basis of its mechanism exposure to the embodiment chokepoint — not on the basis of a buy, sell, or hold call.

Domestic magnet processors

MP Materials ($MP, NYSE). The cleanest US pure-play on the rare earth processing chokepoint. Independence facility in Fort Worth came online at industrial scale Q1 2026 producing NdFeB magnets domestically — the first significant non-Chinese capacity in decades. The 10X facility in Northlake, Texas commissions in 2028, bringing total capacity to approximately 10,000 metric tons per year of NdFeB magnets. Department of Defense holds approximately 10% equity stake post-2025 strategic minerals investment. Apple and General Motors have signed long-term offtake agreements. Disclosure: position taken in 2024-25 and held. The thesis is well-recognized at this point and the stock is at 770x trailing P/E with significant year-on-year appreciation — the entry-point asymmetry is materially diminished from 2024 levels. The structural exposure remains.

Energy Fuels ($UUUU, NYSE). Operates the White Mesa Mill in Utah, the only US facility processing both uranium and rare earth oxides. Heavy rare earth commercial production targeting Q4 2026 with samarium, gadolinium, dysprosium, and terbium output. POSCO collaboration announced for ex-China heavy rare earth supply chain integration. Less crowded than MP Materials as an embodiment-thesis exposure.

Ex-China rare earth refiners (development stage)

NioCorp ($NB, NASDAQ). The Elk Creek Project in Nebraska is a niobium-scandium-rare-earth deposit. EXIM Bank financing decision on a $780 million loan is expected H2 2026 — this is the binary catalyst. Pre-production, meaningful execution risk, but the deposit includes the second-largest dysprosium resource identified in the United States. Significantly more speculative than MP or UUUU.

Japanese actuator and reducer exposure

Nidec ($NJ, NYSE ADR / 6594 Tokyo). Broadest robotics portfolio of the Japanese names — servo motors, Nidec-Shimpo harmonic drives, traction motors for EVs, precision components. US-accessible via ADR. The most accessible Japanese exposure for US retail.

Harmonic Drive Systems (6324, Tokyo Stock Exchange). The premium harmonic reducer leader globally — the company’s name is essentially the category name. Approximately 60% global premium-tier market share. Tokyo-only listing requires an international brokerage account for US retail access.

Nabtesco (6268, Tokyo Stock Exchange). Dominant in RV cycloidal reducers (~60% global share). Tokyo-only listing.

Force-torque sensor exposure

Novanta ($NOVT, NASDAQ). Parent company of ATI Industrial Automation, the global market leader in six-axis force-torque sensors used at humanoid robot wrist and ankle joints. Diversified across robotics, medical, and industrial markets but ATI provides a clean exposure point to the sensor side of the embodiment stack.

Adjacent critical minerals — humanoid-relevant

Almonty Industries ($ALM, NASDAQ). Tungsten producer, not a magnet producer, but tungsten is used in humanoid actuator counterweights and high-temperature alloy components. The Sangdong facility in South Korea commissioned Phase 1 production in March 2026 at ~2,300 metric tons per year of tungsten oxide — the first significant non-Chinese tungsten production receipt in years. Phase 2 is targeting ~4,600 t/yr by 2027.

US retail access notes

$MP, $UUUU, $NB, $NJ, $NOVT, and $ALM trade on US exchanges through standard brokerage accounts. The Tokyo-listed Japanese names (6324, 6268, 6594) require an international brokerage account — Interactive Brokers, Fidelity International, or Schwab Global Account all provide Tokyo Stock Exchange access for US retail.

What to watch

The framework’s next several months hinge on a small number of dated catalysts.

November 10, 2026 — MOFCOM extraterritorial rare earth export control suspension expires. If the suspension is not extended, the October 2025 framework reactivates and the symmetric Pillar 3 instrument goes live. This is the binary date.

Q3 to Q4 2026 — MP Materials 10X facility groundbreaking visible, first significant capex draw, commissioning timeline becomes harder-dated.

Q4 2026 — Energy Fuels first commercial-scale heavy rare earth production. The first non-Chinese commercial-tier dysprosium and terbium output in years.

H2 2026 — EXIM Bank decision on NioCorp Elk Creek $780M loan. Binary execution event for the ex-China heavy rare earth thesis at the next-development-stage tier.

July to August 2026 — Tesla begins Optimus mass production at Fremont per Musk Q1 2026 earnings call guidance. First real Western humanoid scale test.

Mid-2026 to end-2026 — Unitree IPO on STAR Market expected. AgiBot IPO in preparation. Both events will provide audit-grade unit shipment data that the framework currently triangulates from analyst reports.

Where the framework goes from here

The two-clock model becomes a three-clock model. The chip clock and the power clock remain. The deployment clock joins them. All three converge in the same 2027-2030 Goldilocks Window — but each at different resolution speeds and with different geographic chokepoints.

The Substack will track all three clocks in parallel. The chip clock through TSMC, Intel, ASML, SK Hynix receipts. The power clock through transformer supply, SMR commissioning, gas peaker buildout, and grid expansion data. The deployment clock through MOFCOM enforcement, Western humanoid program execution, MP Materials commissioning, and Yangtze Delta supply chain stress-testing.

The thesis isn’t that China wins the AI race. The thesis is the race is bifurcated and the framework needs to track both stacks honestly. The US has the chip wall. China has the embodiment wall. Both walls are real. Both can be partially scaled. Neither can be replaced inside the Goldilocks Window.

That’s the take.

This is framework analysis and educational content only. Nothing in this post is investment advice, a recommendation to buy, sell, or hold any security, or a solicitation. The names mentioned are framework-traceable exposures to the structural thesis, not portfolio recommendations. I may hold positions in any names referenced; positions and views may change without notice. Do your own research and consult a licensed financial advisor before making any investment decision. Past performance is not indicative of future results.

Muscles & Macro — analysis only, never advice.

Very interesting.

I found two stats you brought particularly striking:

NdFeB magnet production (I do wander how quickly MP and the US will be able to catch up), and the complete vertical control in the 200km radius of Shanghai.

In general I think you might be overestimating the value of embodied robots. Maybe important but imo not quite up there with chips and energy.

Quick question - why do you use humanoids as your key metric? I would argue that the significant robots in the future are quite likely not going to be humanoids. But, it's easier to quantify so I guess that.

Also, Tesla's cost (even if we do accept the orojections of when they ramp up production by the end of the year) are all fun and games, but if it's not actually manufacturered end to end at home, doesn't mean much...