The Window

Iran Situation Room

DISCLAIMER: This content is for educational purposes only and does not constitute financial, investment, legal, or tax advice. The views expressed are based on personal analysis and opinion. Markets are volatile, and all trading involves significant risk. You should consult with a qualified financial advisor before making any investment decisions.

In The Last Barrel Standing, we laid out the full Iran thesis — the 18-month pre-depletion setup, the three scenarios, and the investment framework. In The Arsenal Is Empty, we tracked the campaign at Day 17 and confirmed the military degradation was running ahead of schedule.

This is Day 24. Trump postponed strikes on Iranian energy infrastructure this morning for five days, citing “productive” talks with Tehran. Brent dropped 11-15% intraday before recovering to $100. Iran’s state television ran the chyron: “US president backs down following Iran’s firm warning.”

The military campaign delivered. The energy flows did not follow. Here is where the data sits, what changed, and what happens next.

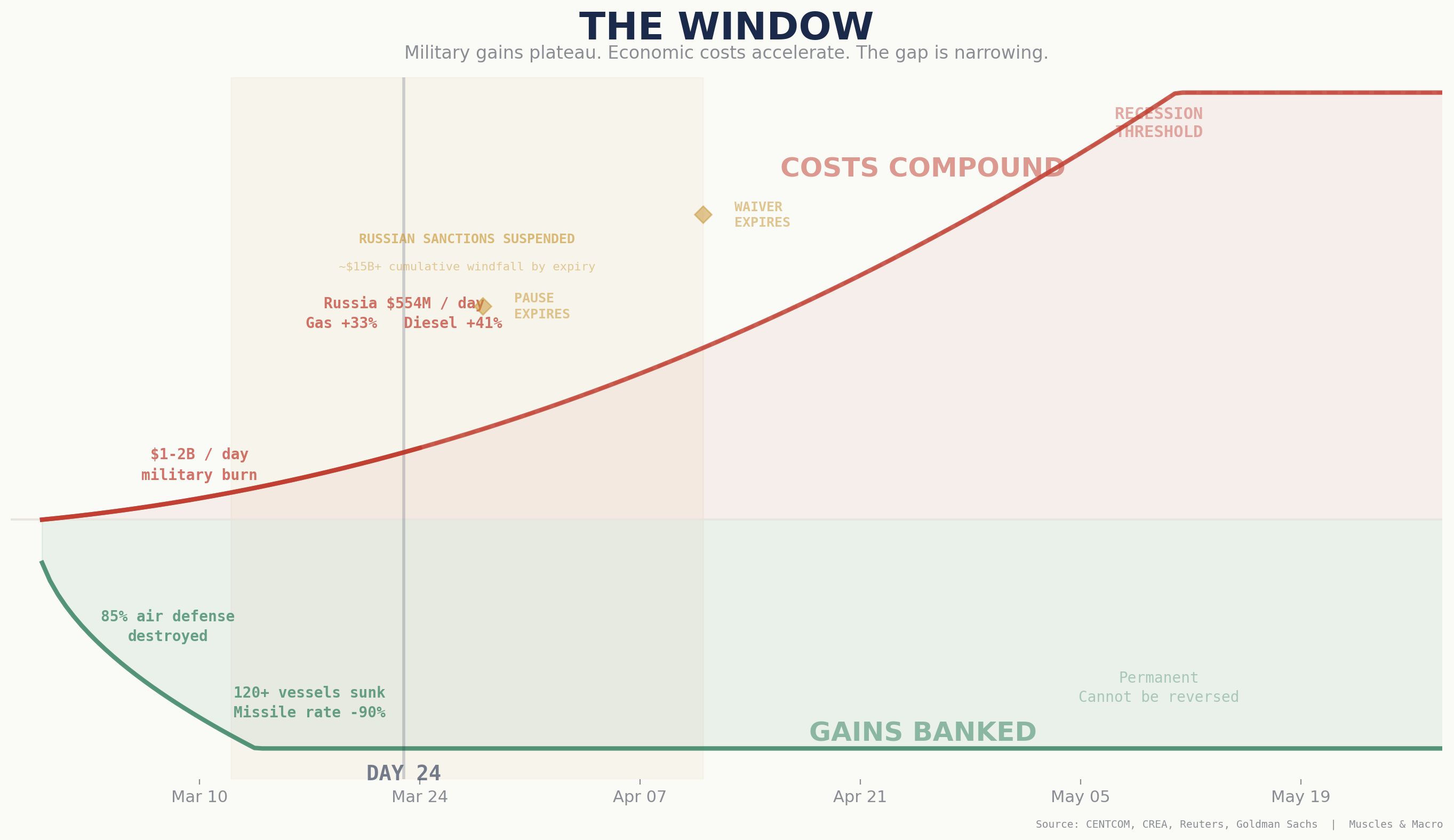

THE WINDOW

There are two curves running in opposite directions right now. One represents the military gains the campaign has banked — permanent, irreversible, accumulating fast in the first two weeks and now plateauing. The other represents the economic costs the campaign is generating — slow at first, now accelerating and compounding daily.

The gap between those two curves is the window. The administration has to convert its military gains into a strategic exit before the economic costs close the gap.

The military objectives have been realized. The campaign killed the Supreme Leader and decapitated the command structure, destroyed 85% of Iran's air defense systems and sunk more than 120 naval vessels, dismantled the proxy network that took forty years to build, and drove missile launch rates down 90% from Day 1 while eliminating most of Iran's mine-laying capability. None of this reverses on a ceasefire.

The economic costs are compounding.. Brent is 41% above pre-war levels even after today’s drop. US gasoline hit $3.96, diesel $5.29. Russia is earning €513 million per day in fossil fuel revenue — up from €472 million in January — because the Bessent 30-day sanctions waiver (issued around March 12, expires approximately April 11) unlocked Russian crude for Indian and Asian buyers while global prices spiked. India doubled Russian crude imports from 1.0 to 2.2 million barrels per day. The Urals discount that three years and $175 billion of Ukraine-era sanctions pressure built has collapsed. The war is costing the Pentagon $1-2 billion per day, and the total is north of $20 billion with a $200 billion supplemental request pending in Congress. Thirteen American servicemembers have been killed. Two hundred wounded.

Every day inside that gap — between military success and economic normalization — costs compound. The administration is simultaneously burning cash, strengthening Russian revenue, depleting the SPR, absorbing consumer damage, and watching Moody’s recession probability approach 50%. The 5-day pause addresses all of these pressures at once: it stops the cost bleed, buys time for Pentagon logistics (the Ford carrier is in Souda Bay for repairs), gives Iran an opportunity to open the strait from a position of collapsing leverage, and gives Trump the framework for a political win. There is no contradiction between these motivations. They all point to the same action.

WHAT THE WAR WAS SUPPOSED TO DO

The campaign had a set of energy objectives that ran alongside the military ones. Deny China access to discounted Iranian crude. Force rival buyers onto market-price supply inside the dollar system. Create the conditions for post-war energy restructuring — IOC re-entry, sanctions relief under controlled terms, the Haifa-to-Muscat corridor. Use the heavy crude supply squeeze to bring Russia into managed reintegration.

None of these can materialize on the current timeline.

Iran is still exporting 1.1-1.5 million barrels per day, down from 2.17 million pre-war but not severed. Reuters confirmed on March 21 that Iranian Light is still trading $8-10 below Brent delivered to China — a discount that actually widened from $6 in September. OFAC has sanctioned zero of the 235+ Iran-linked tankers currently operating. The US authorized a separate 30-day waiver on March 20 covering approximately 140 million barrels of Iranian crude already at sea. The country at the center of the military campaign retained more energy flow control than Iraq (-73% exports), Kuwait (near-total halt), or Qatar (force majeure on all LNG).

China pre-loaded 15.8% more crude in January-February than the year prior. Beijing increased Russian imports, expanded Saudi purchases via the Yanbu Red Sea pipeline, maintained Iranian flows through selective Hormuz transit, and sits on approximately 1.2 billion barrels of strategic reserves — 78 to 108 days of import cover. China’s posture is patience. Absorb costs through reserves and state subsidies, wait for Washington to feel the domestic pressure first.

The Russia reintegration thesis from our March 18 piece assumed the supply squeeze would give Washington leverage to manage Moscow’s re-entry into the global economy. The Bessent waiver was a rational emergency measure — you cannot let global supply collapse during an active war. The problem is the campaign was designed around a 4-6 week window. The waiver was supposed to be a brief, absorbable cost that lapses on April 11 with Hormuz already reopened and Gulf barrels flowing. Instead, the war extended past its anticipated timeline, Hormuz stayed closed, and the temporary waiver became a 30-day revenue pipeline that Russia is maximizing — revenue up, pricing power restored, India doubling imports. The issue is not the waiver. The issue is the campaign could not deliver Hormuz reopening fast enough to make the waiver inconsequential. Every day the strait stays closed, the waiver’s cost compounds.

The energy objectives require a stable price environment to function. The war destroyed that stability. Sanctions enforcement against the Iran-China shadow fleet, activation of the 25% tariff executive order on countries buying Iranian oil, and the full OFAC designation campaign against Iranian tankers all become self-destructive at $100+ Brent because each action removes barrels from a market already in the worst supply crisis since the 1970s.

The 5-day pause is the clearest signal that the administration understands this constraint. The military campaign achieved its objectives. The economic campaign needs the war to end before it can resume.

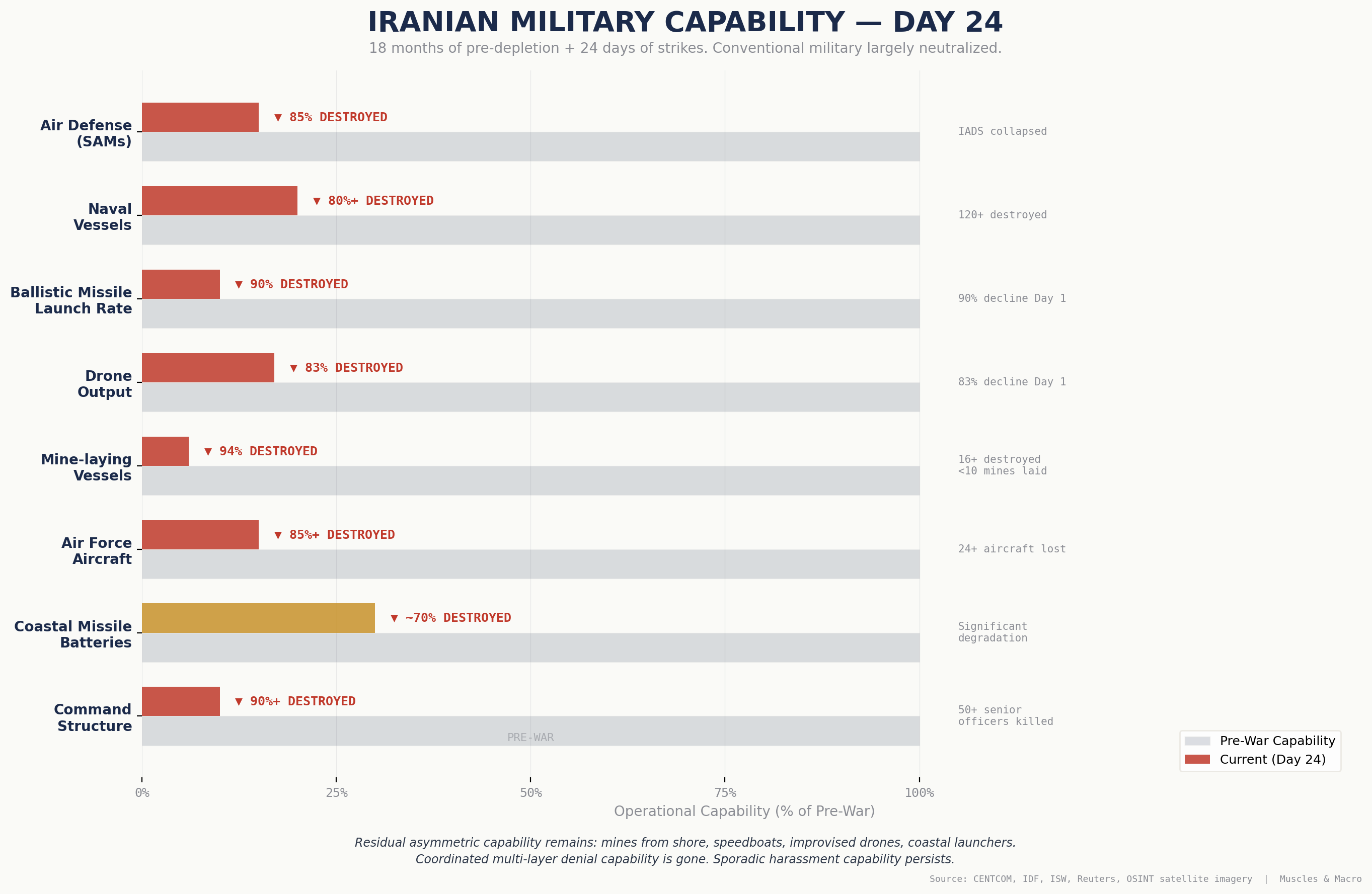

WHAT 18 MONTHS OF PRE-DEPLETION ACTUALLY DESTROYED

The pre-depletion thesis held on the military dimension. 18 months of systematic degradation — Midnight Hammer, proxy elimination, shadow fleet sanctions, economic strangulation, planetary mixer interdiction — meant Iran’s response to the largest joint US-Israeli operation in Middle Eastern history was structurally limited from the first hour.

CENTCOM reported 7,800+ strikes since February 28. Two-thirds to three-quarters of 2,600 mapped military-industrial sites have been hit. The IDF estimates over 6,000 IRGC personnel killed and 15,000 wounded. More than 50 senior military and intelligence officials confirmed dead. 120+ naval vessels damaged or destroyed, including 16 mine-laying vessels near Hormuz. 85% of surface-to-air missile systems eliminated. The integrated air defense system collapsed, giving the coalition complete air superiority. 24+ Iranian aircraft destroyed. Iran’s air force, navy, and conventional missile capability have been functionally neutralized.

Iran’s ballistic missile launch rate declined 90% from Day 1. Drone output declined 83%. No external resupply has reached Iran — no Chinese hardware, no Russian systems, no North Korean munitions. The planetary mixer interdiction from November 2025 holds. Iran is firing from a depleting arsenal with no reconstitution path.

The residual capability is asymmetric, not conventional. Coastal anti-ship missile batteries are significantly degraded but not zeroed — approximately 30% of pre-war capacity remains. Surviving fast boats can still harass. Mines can still be laid from shore or small craft, though the industrial mine-laying fleet is destroyed and fewer than 10 mines have actually been deployed. Midget submarines (Ghadir-class) may still be operational in the strait, though two submarines have been confirmed lost. Iran can conduct sporadic harassment. It can no longer sustain the coordinated, multi-layer chokepoint denial it executed in the first two weeks.

That distinction matters for everything that follows.

WHY THE COERCIVE ARCHITECTURE IS STRONGER THAN BEFORE THE WAR

The enforcement tools the US has available to squeeze Iran’s oil revenue are the same ones that were working before the war started. What changed is the cost of using them.

Before February 28, every enforcement action against Iran carried a three-front retaliation risk: Hormuz closure, proxy activation across the region, and nuclear escalation rhetoric. That combination kept the enforcement calculus frozen for twenty years. OFAC could sanction shadow fleet vessels and banking intermediaries, but Tehran always had the implicit threat of shutting down 20% of global oil trade in response. The uncertainty of that threat — would Iran actually close Hormuz over a tanker designation? — was itself a form of deterrence. It worked because no one wanted to find out.

The war answered the question. Iran did close Hormuz. And now its capability to do it again has been substantially degraded: navy destroyed, mine-laying fleet eliminated, coastal batteries hit, air defense collapsed, proxy network dismantled, nuclear infrastructure buried. The retaliation toolkit that froze the enforcement calculus is either gone or reduced to residual asymmetric capability.

There are six specific mechanisms the US can activate post-ceasefire, each of which is now cheaper to deploy than it was on February 27:

OFAC vessel designations. 235+ Iran-linked tankers are identified but unsanctioned. OFAC adds a vessel’s IMO number to the SDN list, and every port, insurer, classification society, and financial institution in the dollar system cuts it off. The tanker becomes uninsurable, unclassifiable, and unable to dock at any compliant port. The pre-war shadow fleet campaign proved this works — 558 Russian vessels sanctioned, Urals driven from $65 to $40, logistics costs doubled. Post-war, Iran cannot credibly threaten Hormuz escalation in response to tanker designations because the capability to execute that threat is largely destroyed.

Secondary sanctions on financial intermediaries. Treasury was sanctioning Iranian banking networks, front companies, and exchange houses every two weeks from January 2025 through February 2026. The targets: UAE-based exchange houses, Malaysian relabeling operations, Chinese trading companies processing payments. The cumulative effect drove the rial from 430,000 to 1.4 million per dollar, collapsed a major bank, and had IRGC commanders wiring personal fortunes to Dubai. The mechanism operates against the financial ecosystem around Iran, not against Iran directly. It resumes the day after a ceasefire.

Insurance and classification chokepoint. Every commercial tanker needs P&I club insurance (headquartered in London) and classification society certification (Lloyd’s Register, DNV, Bureau Veritas — all Western-based). When OFAC designates a vessel, P&I clubs withdraw coverage and classification societies pull certification. The Hormuz crisis proved how effective this is — war risk insurance removal on March 5 shut down commercial traffic more completely than the IRGC’s missiles did. The same leverage applies vessel-by-vessel to the shadow fleet post-war.

The tariff executive order. Trump signed an EO on February 6 authorizing 25% tariffs on imports from any country purchasing goods or services from Iran. The legal architecture exists and agency authority is delegated. It has never been implemented — activation during the war would have been a simultaneous trade war and energy crisis. Post-war with prices normalized, the enforcement calculus changes. China exports $440+ billion annually to the US. The tariff cost of continued Iranian oil purchases would exceed the savings from the discount by an order of magnitude.

Port state enforcement. The US pressures port states to deny entry to designated vessels. India was seizing Iranian tankers under US pressure throughout 2025. Each port closure raises logistics costs and transit times, eroding the discount economics that make shadow fleet crude attractive. Post-war, port states face lower retaliation risk from Iran for cooperating with US enforcement — Tehran can no longer credibly threaten consequences for compliance.

SWIFT and dollar clearing. The backstop. Iranian banks were disconnected from SWIFT in 2012 and 2018. Iran adapted through bilateral currency arrangements, but these channels are slower, lower volume, and more expensive than dollar clearing. The US cannot prevent yuan-denominated bilateral trade, but it can sanction any institution that facilitates conversion between yuan and dollars on behalf of sanctioned entities.

None of these require Iran’s cooperation. They target the ecosystem — ships, insurers, banks, ports, buyer nations — and let the cost of transacting with Iran rise until the economics break. The war reduced Iran’s ability to impose counter-costs on the enforcers. That is the structural change. The tools are identical. The risk of using them dropped permanently.

SCENARIO UPDATE — DAY 24

The original framework mapped three scenarios. The data 24 days in requires a fourth — Negotiated Exit — which is now the base case.

S1: Negotiated Exit — 40%

Hormuz partially reopens under Iran’s IRGC vetting system. Both sides claim victory. The shooting stops. Oil declines gradually toward $85-90 by end of Q2. The Bessent waiver lapses on April 11 and Russian sanctions pressure resumes. The post-war squeeze architecture activates against a drastically weakened Iran. This is what the 5-day pause is testing.

S2: Prolonged Escalation — 30% (was 15%)

The 5-day window produces nothing. Iran gives no concessions. Strikes resume, potentially targeting power plants. Iran follows through on threats to mine Gulf sea lanes. Oil re-enters the $115-140 range. The recession threshold comes into play. Crack spreads push toward the all-time record. Every energy name in the framework works hardest in this scenario. Defense spending accelerates beyond the $200 billion supplemental.

S3: Fragmentation — 20% (was 35%)

The regime fractures under sustained bombardment and economic collapse. No unified government emerges. IRGC provincial commanders become regional power brokers. Khuzestan contested. Iranian barrels go offline for years. IOC re-entry and corridor thesis deferred to the 2030s. Supply denial thesis gets stronger — fragmented Iran produces even less than sanctioned Iran.

S4: Controlled Transition — 10% (was 25%)

Clean regime change. Pahlavi or reformist coalition. Sanctions unwind. IOCs re-enter. Full thesis payoff on a 12-24 month timeline. The maximum-upside outcome that remains structurally possible but unsupported by the current data. No clean transition path is visible with the opposition fragmented and Mojtaba installed.

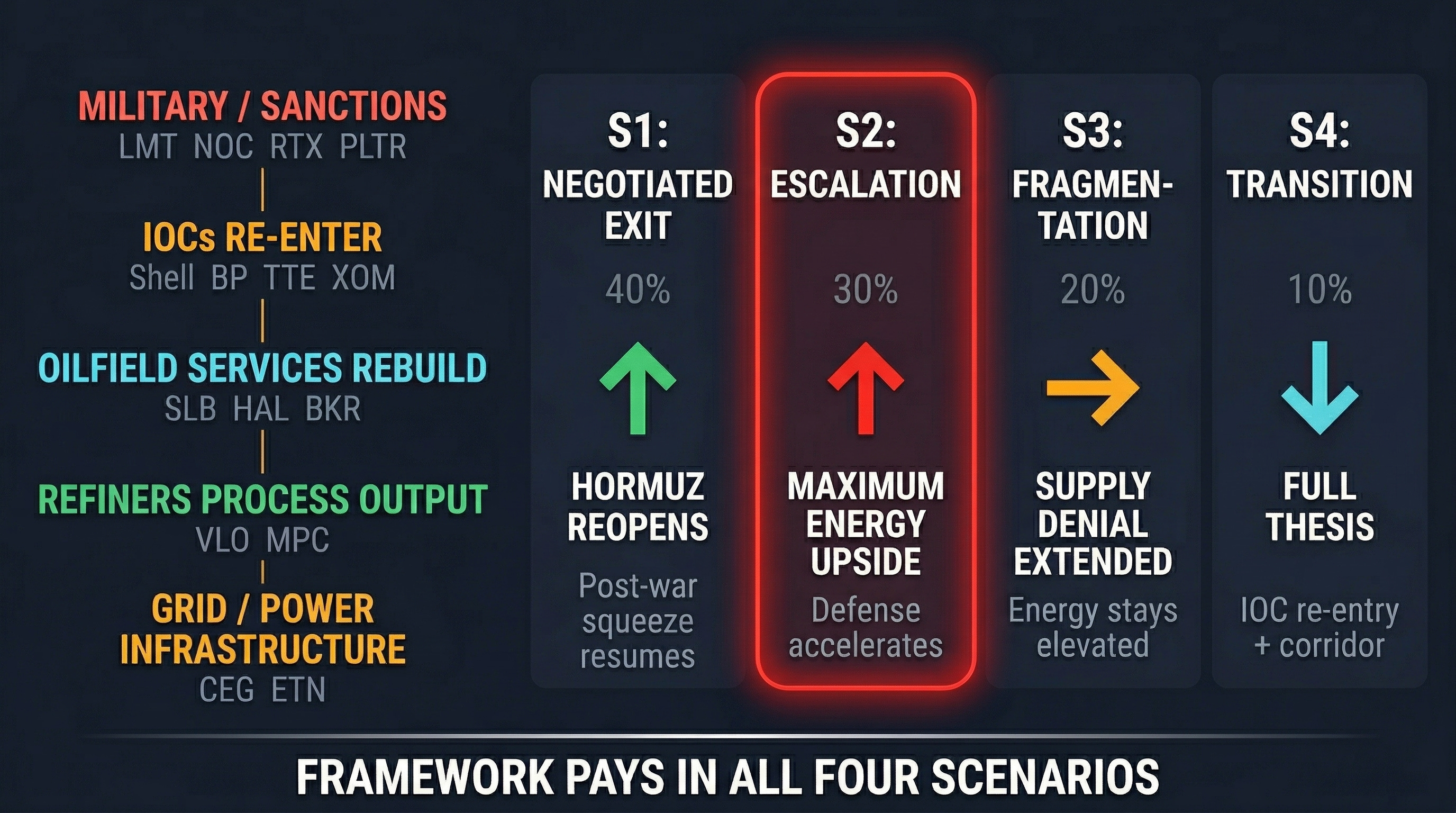

WHERE THIS LEAVES THE FRAMEWORK

The framework from The Last Barrel Standing was built to pay across multiple scenarios. That structural logic holds — the magnitude and timeline shift depending on which path materializes, but the corporate hierarchy maps to the right sectors in all four outcomes.

Gulf Coast refiners with Western Hemisphere feedstock remain the cleanest positioning in the framework regardless of scenario. Crack spreads at $58 per barrel — triple pre-war norms — reflect the structural advantage described in every prior piece. On March 23, oil dropped 13% and Marathon Petroleum closed up. The mechanism is operating exactly as modeled.

Integrated energy majors carry crude price beta that varies by scenario but maintain long-term supply control positioning that strengthens under any post-war resolution. LNG is structurally underappreciated given Qatar’s force majeure and the months-to-years restart timeline — US LNG exporters are filling a gap that persists across every outcome. Defense spending is committed through the FY27 cycle regardless of how the war resolves — the $200 billion supplemental, the restocking orders, and the procurement acceleration are locked in.

The longest-dated layer — oilfield services and IOC re-entry — requires post-war stability and a functioning counterparty in Tehran. That timeline extended. The oil is still in the ground. The infrastructure still needs replacing. Patience is required.

Scenario-specific positioning adjustments, timing considerations, and the risk management structure across the probability matrix will be covered in the paid tier when it launches. The free column maps the framework and the probabilities. The paid tier will map the execution.

WHAT TO WATCH

March 28. The only signal that matters is Hormuz transit volume. If more tankers transit, the off-ramp is real. If transit stays at the current trickle, the cycle restarts.

Brent over the next 48 hours. Rebound above $110-115 by midweek means the money doesn’t believe the talks. Holds below $105 means real capital is betting on resolution.

April 11. The Bessent waiver expiry is the most important economic decision point in the next three weeks. If Hormuz is open, the waiver lapses and Russian sanctions resume. If Hormuz stays closed, the waiver extends and Russia keeps earning half a billion dollars a day.

Iran mine-laying. Iran’s Defense Council threatened on March 23 to mine Gulf sea lanes if coasts or islands are attacked. Any detected mine-laying activity overrides the diplomatic window immediately.

Detailed signal tracking, scenario probability adjustments, and the positioning framework across scenarios will be available in the paid tier. The free column gives you the thesis, the data, and the probabilities. The paid tier gives you the operational detail.

This content is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Markets are volatile and all trading involves significant risk. Consult a qualified financial advisor before making any investment decisions.